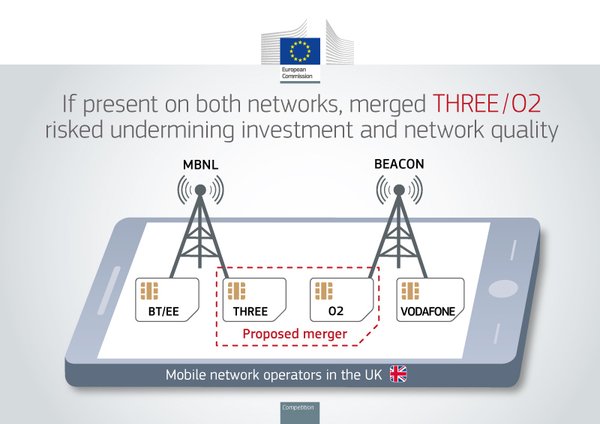

Hutchison/Telefónica UK blocked: BT wins, all the others lose. What lessons for competition law and regulation?

The prohibition of the Hutchison/Telefónica UK deal, which has been made official earlier today (see here), is a bit like Leicester City winning the Premier League. As the months passed, the impossible became likely, up to the point when it was certain that it would actually occur. So no big news today, as the only remaining question was when the decision to block the deal would be announced.

While we wait for the decision to be published, I can think of a couple of issues for discussion:

- The Commission powers in horizontal merger cases – law or discretion?: The Commission has the power to block horizontal mergers in a very broad range of scenarios. ‘Four to three’ mergers in telecoms markets illustrate this very well. The Commission does not need to establish (single or collective) dominance to block a merger between competitors (or non-competitors, for that matter). In the so-called ‘gap’ cases, it is enough to show that some parameters of competition will be significantly affected by the transaction.

This background is useful to understand why some commentators have started to ask whether the Commission has in fact too much power in horizontal merger cases, in particular in ‘gap’ ones. James Venit has recently written an article making this point (see here). Can the Commission prohibit just any horizontal merger it wants? It may be the case that the reasons to block Hutchison/Telefónica UK were compelling. The outcome may be perfectly sound. However, the decision might fuel the debate in this sense.

I see where the arguments of these commentators come from. The assessment of unilateral effects in merger cases is the privileged realm of the so-called ‘complex economic assessments’. Intervention depends on forecasts about post-merger effects (which, again, may be perfectly accurate).

The problem with ‘complex economic assessments’ is that they come with a ‘margin of appreciation’, and with a ‘margin of appreciation’ comes limited judicial review. Is it then a matter of discretion, and not of law, as it is in theory and it is meant to be? I guess it would probably help if the EU courts defined a set of principles and proxies for the assessment of mergers in ‘gap’ cases at some point.

- BT is the big winner: The overall effect of a series of individual decisions has been to tilt the game in favour of BT. After the acquisition of EE, BT is the only truly integrated operator in the UK. It has the largest fixed network and is the leader in retail mobile and fixed broadband. This landscape is not necessarily problematic in itself, but it is probably not ideal either.

Of the series of decisions that have been adopted in the past few years, there is only one that I would qualify as ‘manifestly incorrect’. I have written about it a few times (see for instance here). Some of you may remember that Ofcom created a brand new doctrine of non-essential facilities to force Sky to supply its premium sports channels to its rivals, including BT. In doing so, it neutralised an important source of competitive pressure. BT’s life is much easier after this decision, and the ability of Sky to challenge the position of the incumbent has been significantly impaired.

Some of you might react by saying that this obligation was formally removed in November last year. Well, yes and no. If you take a look at it, you will see Ofcom wrote something along the lines of: ‘I remove the duty to supply, but you better continue supplying’. Once an obligation to supply is imposed, it is likely that it is there to stay. Which is probably why the debate about interim measures has also become popular. My guess is that many people have the secret hope that a quick and dirty provisional measure will become permanent (it works for Uber when it enters new cities, so I guess some people have figured out it could work elsewhere).

Pablo, did you have a problem with the BT call center recently?

Kidding aside, I totally agree with your comment on how the Commission has almost carte blanche (“almost” as in limited judicial review) for gap cases. The Commission can just state that innovation will be affected. In practical terms, the case team focuses on internal documents of the parties on their pipeline projects. Every company magnifies their own projects, that’s the work of the corporate marketing teams. The Commission relies on this (as well as the hostile comments of competitors, and the customers responses to the Commission’s questionnaires “yes, why not”) to prove the effect on innovation. The problem lies with the practical methodology of assessment of mergers, not only with the legal test.

And agreed on how vertical integration can prove as bad as fewer players on the market. Sometimes competition law decisions tend to categorize the business world in horizontal and vertical effects. But vertical integration can also affect an horizontal assessment.

Someone has pointed to the less choice (and higher prices?) of books in Italy after the Mondadori/RCS deal because of the vertical integration of the post-merger entity. Food for thought (which reminds me I need to go to dinner).

Gianni De Stefano

11 May 2016 at 7:38 pm

Haha

Full disclosure, dear Gianni: I am a proud user of BT’s flawless retail services, and have been one since I arrived in London in 2010!

Pablo Ibanez Colomo

11 May 2016 at 8:12 pm